As an independent insurance broker or agent, you generate your “bread and butter” from selling insurance to small businesses. No matter what niche you serve, you can rest assured that current reports show a vibrant and healthy U.S. small business economy.

Your Growing Market: A Look at the Numbers

The U.S. Small Business Administration and the U.S. Bureau of Labor Statistics recently shared some compelling numbers about business growth in the United States. A quick look at these facts and figures shows that your target market is growing.

The May 2018 Detailed Industry Employment Analysis showed:

- Nonfarming employment in all major sectors and target classes continues to trend upwards (as of June 2018).

- These positive trending sectors include retail trade, education and health service, construction, professional and business services, transportation, private education and health services, and leisure and hospitality.

The 2018 Small Business Profile showed:

- Over 500,000 new businesses are started each month in the U.S.

- There are 30.2 million small businesses with 58.9 million employees.

- With 99.9% of US businesses classified as small, they provide jobs for 47.5% of the nation’s employees.

Translation: Your target market needs to hear about what you have to offer and how it can help them. Do the business owners you work with know what they may need?

Educate About Small Business Insurance Options

It is a fact that every business needs insurance. It is your job to educate prospects about the options they need to consider. Many owners are so laser-focused on the day-to-day operations that they forget about easy ways to protect their assets.

Here is an FAQ you can share with your customers to quickly spell out the big picture. (Download a free PDF you can share with prospects.)

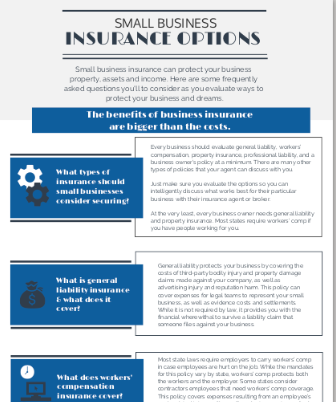

What types of insurance should small businesses consider securing?

Every business should evaluate general liability, workers’ compensation, property insurance, professional liability, and a business owner’s policy at a minimum. There are many other types of policies that your agent can discuss with you.

Just make sure you evaluate the options so you can intelligently discuss what works best for their particular business with their insurance agent or broker.

At the very least, every business owner needs general liability and property insurance. Most states require workers’ comp if you have people working for you.

What is general liability insurance and what does it cover?

General liability protects your business by covering the costs of third-party bodily injury and property damage claims made against your company, as well as advertising injury and reputation harm. This policy can cover expenses for legal teams to represent your small business, as well as evidence costs and settlements. While it is not required by law, it provides you with the financial wherewithal to survive a liability claim that someone files against your business.

What does workers’ compensation insurance cover?

Most state laws require employers to carry workers’ comp in case employees are hurt on the job. While the mandates for this policy vary by state, workers’ comp protects both the workers and the employer. Some states consider contractors employees that need workers’ comp coverage. This policy covers expenses resulting from an employee’s work-related injury or illness. From lost wages to medical expenses and legal fees for lawsuits, this policy is a win-win for the business owner and employee when the time comes to file a claim.

What is property insurance for business?

Whether you lease or own your building, or even work out of your home — business pottery insurance protects your company’s physical assets from disasters like theft, fire, explosions, and storms. Whatever you need to run your business—computers, documents, equipment, inventory, and even fencing—property insurance is designed to cover lost, stolen and damaged property, and even loss of income from that property damage.

What is professional liability insurance?

While General Liability covers your business when a third-party sues your business over bodily injury or damage, Professional Liability is more like malpractice insurance. This type of insurance is designed for people who make a living off of their expertise. This policy kicks in when a third-party sues you for providing negligent professional services, not upholding contractual promises, providing incomplete work, or making mistakes.

What is a business owner’s policy (BOP)?

In layman’s terms, BOP insurance is an affordable insurance package that bundles together liability and property insurance. Your agent can walk you the options that make the most sense for your particular situation.

Can professional liability and general liability policies cover the same claims?

No. The policies cover different types of liabilities and risk exposures. General liability focuses on physical damages, while professional liability covers third-party financial losses.

Do I need both property and liability insurance?

The policies are designed to protect a small business with coverage that includes:

- liability coverage from interacting with the public, and

- damage or loss to physical assets the business relies on for conducting business.

What happens if I don’t have business insurance?

Insurance is protection for the future. No one knows when an accident, lawsuit or disaster may strike.

Here are two facts to consider:

- Dependent upon the products and services you provide, most clients seek to work with businesses that have coverage for losses that may occur as a result of your work.

- The majority of states require workers’ compensation insurance for businesses that have people who work for them. (Some states even consider contractors as employees, which requires workers’ comp coverage.)

The benefits of business insurance are bigger than the costs. Why leave the future of your business to chance?

Download this FAQ as a free PDF you can share with your prospective clients now.

Download Small Business Insurance FAQs